Leading Economic Index Falls For 16th Straight Month

-

-

Published Friday, August 18, 2023 at: 8:27 PM EDT

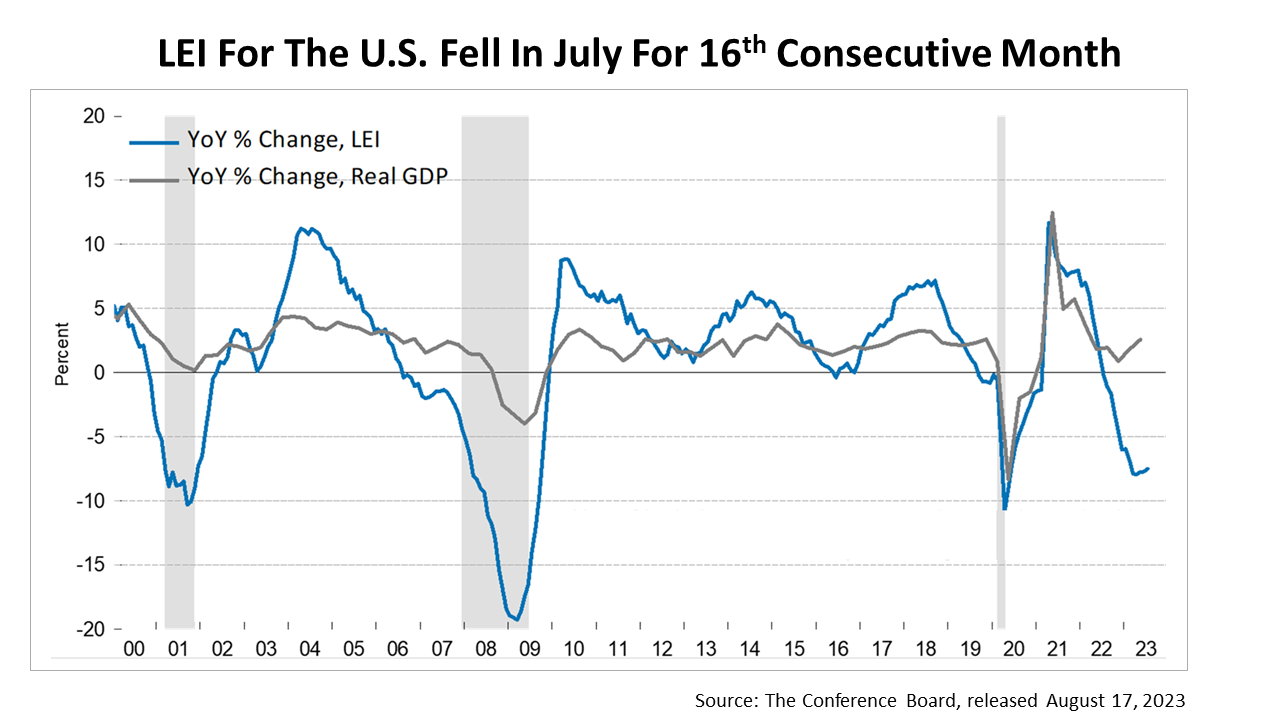

The Leading Economic Index (LEI) for the U.S. declined for the 16th consecutive month in July. “The leading index continues to suggest that economic activity is likely to decelerate and descend into mild contraction in the months ahead,” according to The Conference Board’s (TCB) data release on August 17. TCB is now forecasting “a short and shallow recession in the Q4 2023 to Q1 2024 timespan.”

TCB’s forecast for a recession in the near-future is a big story. TCB is a credible institution. TCB is an association for the world’s largest companies. It has collected, calculated, and published the LEI and its 10 subcomponent indexes for decades and employs a team of economists who have made the LEI a reliable predictor of every recession in modern U.S. history – except for the anomalistic Covid-19 recession. Thus, TCB’s forecast mistake is important to understand.

Things started to go wrong on July 21, 2022, when TCB for the first time in 14 years predicted a recession would begin at the end of 2022. It was a sudden about face. Just a month earlier, in June 2022, TCB had predicted a 2.3% U.S. growth rate for 2022. However, TCB suddenly reversed itself when its index of Leading Economic Indicators for the U.S. declined for the third month in a row. On July 21, 2022, TCB forecasted: “US recession around the end of this year and early next is now likely.”

A year later, with no recession in sight and robust growth widely expected for the rest of 2023, TCB has pushed back the recession start-date to the fourth quarter of 2023 or the first quarter of 2024.

Why has TCB’s forecast for a recession been wrong? Fritz Meyer, an independent economist, says the U.S. economy changed in recent decades but the LEI did not, and the manufacturing subcomponents are overweighted in the LEI index. The manufacturing sector of the economy accounts for only 10% of U.S. gross domestic product (GDP), while service-sector businesses account for 90% of GDP. The list of the 10 LEI subcomponents below highlights the influence of manufacturing in the LEI:

1) average weekly hours worked, manufacturing

2) average weekly initial unemployment claims

3) manufacturers’ new orders – consumer goods and materials

4) ISM index of new orders

5) manufacturers’ new orders, nondefense capital goods

6) building permits – new private housing units

7) stock prices, S&P 500

8) Leading Credit Index™

9) interest rate spread minus fed funds

10) index of consumer expectations.

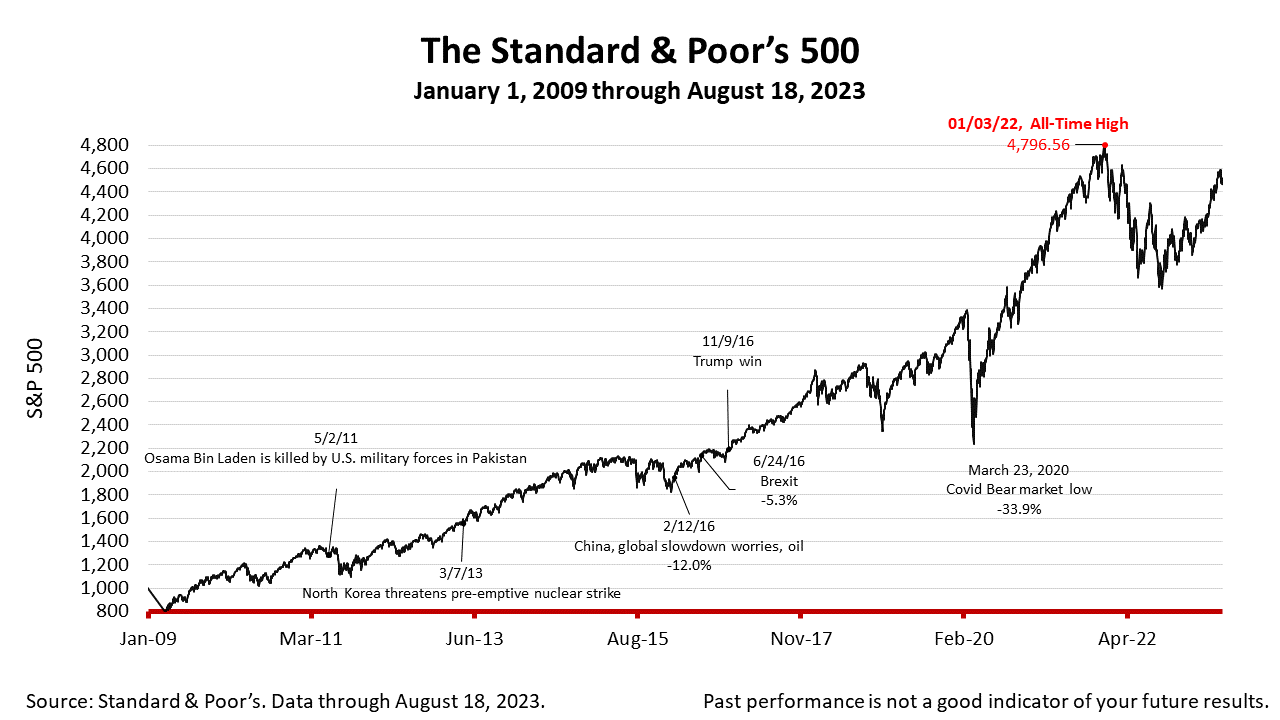

The Standard & Poor’s 500 stock index closed Friday at 4369.71, down -0.01% from Thursday, and -2.11% lower than a week ago. The index is up +95.30% from the March 23, 2020, bear market low and -8.90% lower than its January 3, 2022, all-time high.

The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is a market-value weighted index with each stock's weight proportionate to its market value. Index returns do not include fees or expenses. Investing involves risk, including the loss of principal, and past performance is no guarantee of future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation, or advice of any kind, and it is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Tax advice always depends on your particular personal situation and preferences. You should consult the appropriate financial professional regarding your specific circumstances. The material represents an assessment of financial, economic and tax law at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions. This article was written by a professional financial journalist for Advisor Products and is not intended as legal or investment advice.

This article was written by a veteran financial journalist based on data compiled and analyzed by independent economist, Fritz Meyer. While these are sources we believe to be reliable, the information is not intended to be used as financial advice without consulting a professional about your personal situation. Indices are unmanaged and not available for direct investment. Investments with higher return potential carry greater risk for loss. Past performance is not an indicator of your future results.

2024

-

Stocks Closed At A Record High

Stocks Closed At A Record High

-

Federal Reserve Projects Strong Growth

Federal Reserve Projects Strong Growth

-

The Best People Were Wrong

The Best People Were Wrong

-

This Week’s Investment News In Six Charts

This Week’s Investment News In Six Charts

-

U.S. Investor Picture Of The Week

U.S. Investor Picture Of The Week

-

The Conference Board Backs Off Its Recession Forecast

The Conference Board Backs Off Its Recession Forecast

-

Softening Economic Data, Inflation Fears Dampen Stock Rally

Softening Economic Data, Inflation Fears Dampen Stock Rally

-

S&P 500 Closes Above 5000 For The First Time Ever

S&P 500 Closes Above 5000 For The First Time Ever

-

Why America Is The World’s Economic Leader

Why America Is The World’s Economic Leader

-

Investment News For The Week Ended Friday, January 26

Investment News For The Week Ended Friday, January 26

-

Why Stocks Broke The All-Time Record High

Why Stocks Broke The All-Time Record High

-

A Strategic Update, With Stocks Near All-Time High And Crises Unfolding

A Strategic Update, With Stocks Near All-Time High And Crises Unfolding

")